Sweet or Sour? Candy Co. Doubling Rev YoY at 6x NTM P/E ($SOWG)

If freeze dried candy (FDC) has staying power, Sow Good is one of the cheapest food and beverage stocks available, and should be trading at $20+.

Sow Good Inc. (SOWG) is a freeze dried candy company that uplisted from the OTC to the Nasdaq on May 2nd. The market is largely unfamiliar with the name. It has grown revenues at a 200% CAGR over the past several years and 2024E revenues have been implied to be over 4x 2023’s. The company has paid off its debt and trades at a NTM P/E of slightly under 6x. At first pass execution has been exceptional—aside from a recent capital raise—and the stock is far too cheap. For more background read DA Metropolitan’s great writeup summarizing the situation. After an initial melt-up, the stock price has round tripped after up-listing to the Nasdaq. At time of writing it trades at $10.5.

Is the selloff justified? The main arguments are as follows:

FDC is a fad and there is not a solid business ex-hype

FDC will be subject to commodity-like price competition

Management won’t execute and or are untrustworthy

Given such optical cheapness—and that both uplist and raise are behind us—it’s a sensible time to evaluate these claims.

Overview

Sow Good was founded in 2010 by (married) serial entrepreneurs Claudia and Ira Goldfarb. Previously they founded a freeze-dried dog treat company, scaled it, and sold to PE. Freeze-drying is a process in which products are frozen at low temperatures and then ice is removed through sublimation. If you’ve had “astronaut food” you’ll be familiar although I can attest FDC is far better.

Sow Good owns ~50k of warehouse space and contracts with several packaging companies to produce its products. Last year it sold ~14 million units. The company uplisted predominately for better visibility and access to capital, which will allow it to solidify its first mover advantage. From this, they’ve raised around $12.8m after fees. The money will be invested in expanding manufacturing capacity to meet demand, and likely into some viral marketing as well, since this is a lever the company has yet to pull.

Is FDC a Fad?

To me, products are fads when there is no enduring value to consumers beyond the trend itself and/or when there is no brand identity. Yet conspicuously absent amongst online investor discussion of Sow Good is an actual analysis of its products. I ordered several different items from Amazon. Obviously this is subjective—but there is something here.

Unlike “astronaut food”, FDC is a legitimate value-add. It tastes great. For anyone with TMJ issues traditional chewy candy is a no-go, but FDC is fine. Also the mouthfeel afterwords is also far better—FDC does not stick to teeth or braces.

Therefore, for parents and dentists concerned about children’s oral health, it’s reasonable to expect FDC to have some staying power. Much of the marketing around FDC leans into this. I talked with an orthodontist who confirmed there’s discussion in the community about this trend, and that providers have been recommending FDC as a better alternative. Surprisingly 31% of children between 2-18 eat candy every single day, and consumption preferences often last a lifetime. If Sow Good is the brand of choice for FDC—a possibility given their execution so far and superior retail presence —it may demonstrate more staying power than it is being given credit for.

Freeze dried candy is incredibly gentle on teeth. Unlike hard or sticky candies that can pose a risk to dental work or sensitive teeth, freeze dried candy melts in your mouth without requiring excessive chewing or biting force. This minimizes the risk of damaging braces or causing discomfort. [Source]

Even if FDC is a fad in the sense that the hype which has recently gained momentum will soon reverse, it could still be substantially undervalued. It is highly unlikely revenues are anywhere near peak.

Evaluating Fad Stage

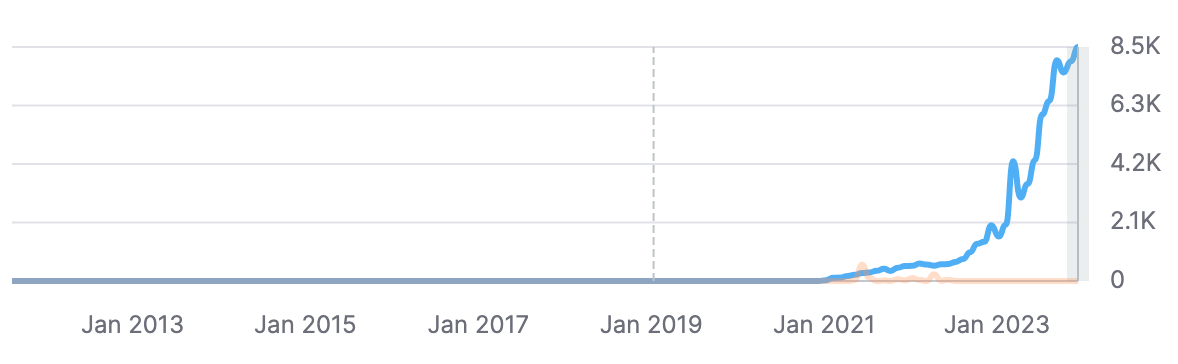

If one naively looks at the general Google Trends data for FDC, it appears to be in decline since late 2023:

This actually seems positive for Sow Good vs. competitors as its website views have continued on a hockey stick trajectory. Importantly the traffic is entirely organic.

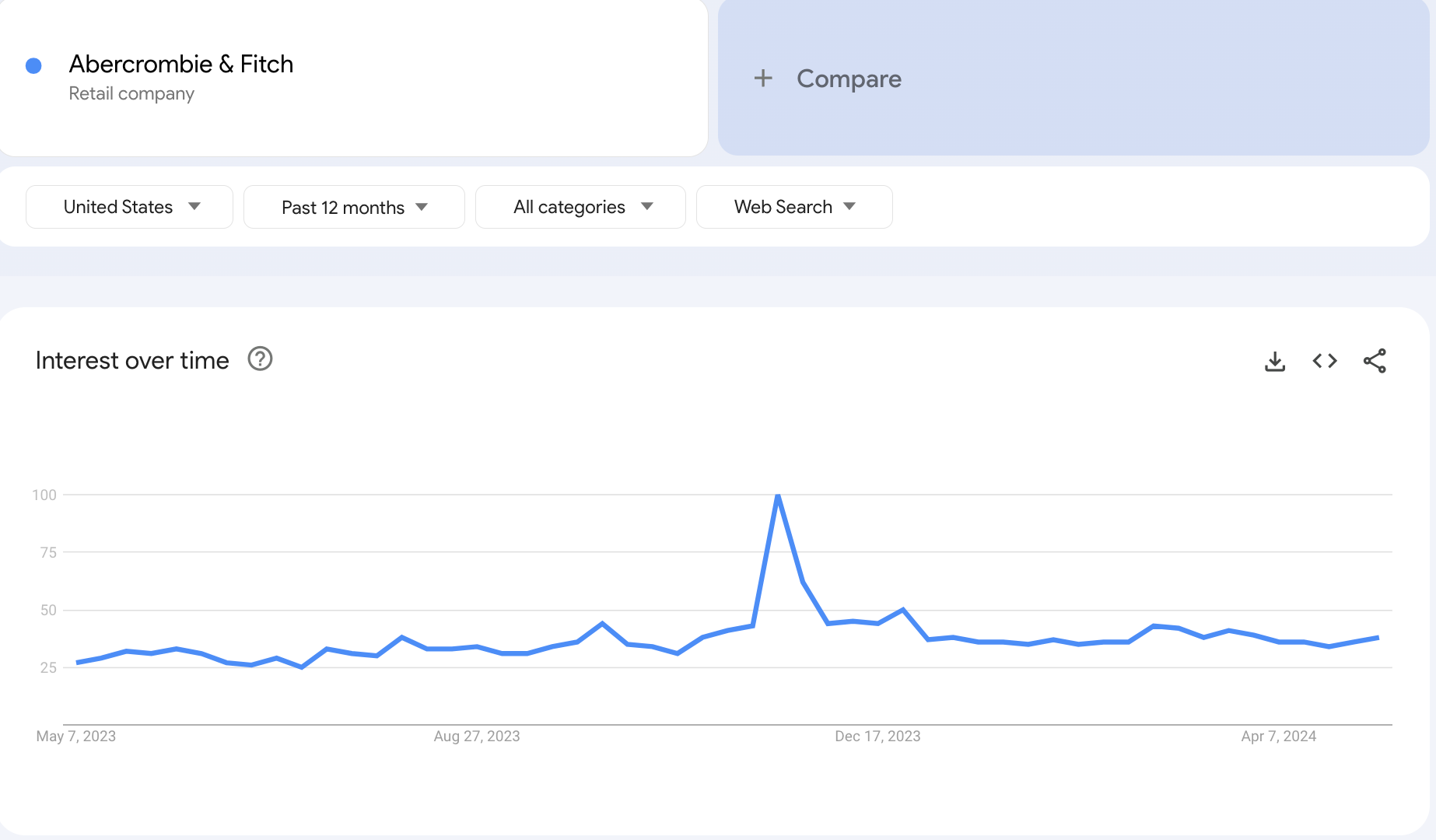

When a company has enduring consumer appeal, revenues can continue to accelerate long beyond when a trend has peaked. While not at all an analogous company, consider that ANF 0.00%↑ has continued to grow revenues after public interest peaked last year (per Google trends). Abercrombie has leaned into manufacturing apparel “essentials”, so it’s not as if there are no substitute brands—in fact, they’ve removed their once-iconic branding from their clothes almost entirely.

Growth Potential

Obviously growth has been strong—but there are several levers for Sow Good, mostly centered around advertising, that the company has yet to pull. It’s interesting to see Sow Good’s complete lack of a corporate TikTok presence, which is massively important for many upstart candy companies, like Poppin.

Similarly, the company tells us that “video reviews of SowGood’s products that are organically generated by TikTok users have amassed over 4.5 million views as of December 31, 2023.” This is barely anything.

Consider the following FDC video from a single influencer which has almost 10 million views. Upon investigation, the rates for several influencers in the space come out to a range between $10K and $20K depending on the specific account. This is well within Sow Good’s SG&A budget post-raise; I’d encourage them to dedicate far more to marketing on TikTok.

The company is also generally able to lean into e-commerce to a greater extent. Per the S-1, “we sell our treats across retail, wholesale distributors, and online e-commerce channels, which comprise 63%, 34%, and 2% of our sales through the third quarter of 2023, respectively.” For a traditional candy company this would make sense, but for one in hyper-growth supported by virality, it represents a strong opportunity. If new converts initially try a product they buy on TikTok shop, enjoy it, and later see the product in a retail store, that is a strong “onboarding process”.

The main growth opportunity is expanding via store partnerships. Currently, Sow Good is in Circle K (2,000 stores), Cracker Barrel, Five Below (all 1,550 stores), and SESCO (300 convenience stores). Launches are pending in Party City, Kroger, 7-Eleven, Dollar General & Hobby Lobby. Importantly the company is rolling out in Target and is guiding for presence in 1,859 stores by June ‘24. Consider the following:

“Merely by meeting the current level of demand for our treats, we anticipate our net sales surging exponentially. To try to meet this demand, we have increased our workforce sevenfold since March 2023, transitioned to a 24/7 production cycle, and leased 62,000 square feet of warehousing space in the Dallas metroplex to be able to scale and streamline distribution. In addition to scaling production of our four freeze driers as of February 10, 2024, we are in the process of building two additional freeze driers for our Irving facility. We anticipate these additional two freeze driers being operational in the first half of the calendar year 2024.

The company discloses that their 2024 production capacity will reach 30 million units as a result of the above initiatives. The company reached $9m in Q4 revenue selling 2.1m units per their most recent investor presentation. If they hit capacity, which they have said demand outstrips, they are “guiding” that they should hit at least $75 million in 2024.

Is FDC commodity?

While Sow Good has an obvious first mover advantage, there are valid concerns that traditional companies or other FDC startups could enter the market. The latter is less likely to be a threat than the former. Consider the following:

“SowGood spent over two years and over $10.0million dollars to develop a state of the art manufacturing facility and freeze drying equipment calibrated specifically for our products prior to the commercial launch of our freeze dried treats.”

“Manufacturing our treats requires careful handling so as to protect the integrity of theircrunch factor,a characteristic of freeze dried candy… the technical knowledge and expertise required to build a freeze drier facility matching our current capacity poses a substantial barrier to entry for competitors in the confectionary space.”

Given its raise, retail relationships, and Nasdaq listing, Sow Good is primed to outcompete smaller players. Conversely larger companies move slowly and I’d anticipate several more quarters go by—during which Sow Good would continue to compound revenues—before they take notice. In any case, price competition has not yet largely begun per Amazon data of a variety of FDC options:

Valuation

A simple projection of how Sow Good’s 2024 financials shows the opportunity. Capacity is the main constraint, and management has said it should grow to ~30 million units as more capacity comes online throughout ‘24. Relatedly, in H2 24 I expect slight margin improvements due economies of scale:

This would give an NTM P/E of just under 11x. But if shares stay in the $10s post-capacity buildout, it likely the NTM P/E for Q4 ‘24 would be low single digits. Based on this, if investors can get comfortable with the story, the company should be trading at somewhere closer to $20-25 today. Tomorrow’s Q1‘24 earnings will provide an important datapoint.

Large and relatively mature/stagnant candy companies like HSY 0.00%↑ and TR 0.00%↑ trade at 21.93x and 35.33x though obviously their size and brand recognition contributes to their multiple. Savory snack-maker BRID 0.00%↑ trades at 24.9x, which seems overvalued considering they forecast revenues declining. JBSS 0.00%↑, which sells nut-based snacks (a similarly low-moat industry) expects a mere 5% revenue CAGR growth yet is trading at 21x NTM P/E. Why is SOWG 0.00%↑ where it is?

Capital Raise and Risk Factors

Current valuation is taking into account the fears discussed earlier, which appear overblown to me. But there is a more justifiable overhang due to management’s capital raise post uplisting.

There are two main reasons to uplist from the OTC: eyeballs and liquidity. Broker-dealers are averse to running afoul of FINRA and will not touch most companies trading on the OTC. Similarly, managers will not invest their client funds into OTC companies. That Sow Good chose to uplist demonstrates they believe this is a time when investor awareness and liquidity is paramount given their first mover advantage. They tell us as much:

“Sow Good intends to use the net proceeds from this offering for general corporate purposes, which may include capital expenditures for the expansion of production capacity, funding working and growth capital, the expansion of the Company’s sales and marketing function, and the reduction of certain tranches of indebtedness.” [Source]

The company now has $12.8 million to work with. It does seem hasty to have priced the offering at $10 when shares were trading far higher at $22. For what it’s worth, the IPO book runners have bought their over-allotment of shares reinforcing that prices today are too cheap:

I do think the raise was poorly executed, but I will note that the company’s lack of free float makes it more likely to have drawn the ire of Nasdaq prior to uplist, so perhaps it is a “reward” for Roth and Craig Hallum. For more on this, please listen to this excellent Planet Microcap podcast.

It’s also the case that the management team are simply inexperienced in the public markets. This is a risk factor but also a mitigating factor insofar as it explains this raise. In terms of actually putting the money to use, it is an excellent time to have more capital than competitors:

"With no major direct competitors in the freeze dried candy space... we are capitalizing on our early mover advantage and rapid scaling experience to become the dominant player in this fast growing market."

Besides the “hype” related risks already addressed, there is notable key person risk given the company’s unique ownership. Though clearly competent entrepreneurs it likely does not please the market that the company’s chairman and CEO are married—although of course I wish them the best of health and luck!

Ownership

Incentives are extremely aligned with directors and executives (mostly the Goldfarbs) owning a staggering 90+% of shares. As the equity hit certain volume and price levels, various tranches of warrants owned by the Goldfarb’s were exercised resulting in around $10m of shares being issued. Notably “the Company’s debt was reduced by $5,200,362.50” meaning that insiders used a substantial portion cash to pay off the company’s debt.

I would note that all the risk factors of FDC are present with freeze-dried dog treats, and yet the Goldfarb’s were successfully able to scale and execute. Prior success at a highly comparable situation—with similar challenges—is reassuring.

Conclusion

The company has undergone its first roadshow, has received positive coverage from its bookrunners, has cash to invest into meeting demand and viral marketing, and has the strongest retail partnerships in the burgeoning FDC space. The Goldfarbs are extremely incentivized, likely putting a majority of their net worth on the line. They’ve executed before in a highly analogous space with similar “fad” and competition risks.

If you listen to management and believe their projections, this is a $20+ stock at least—which, by the way, is where it traded before a reasonable yet perhaps naive business decision to solidify its first mover advantages through raise. If we can forgive that I’m inclined to say “so far sow good.” Tomorrow’s earnings call will be extremely interesting.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered investment advice. Investing involves risk, including the potential loss of principal. The author holds a material position of the security discussed. The author is not a registered investment advisor and does not provide personalized investment advice. Always conduct your own research and consider your investment objectives and risk tolerance before making any investment decisions. The author and publisher shall not be liable for any actions taken based on the information provided in this article.

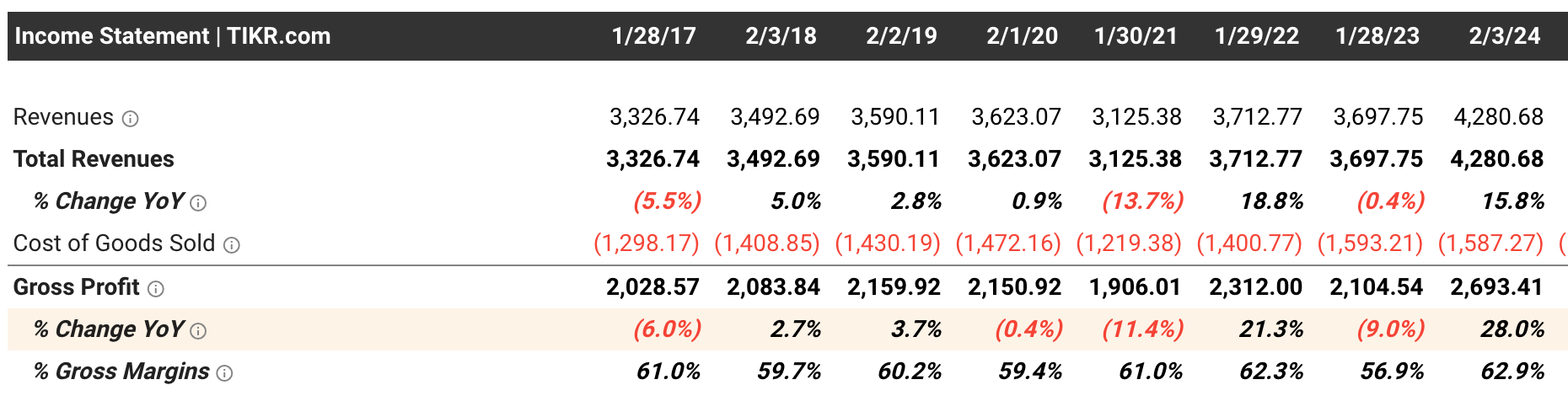

In March Investor deck, they disclosed selling 2.1 million "units" in Q4 2023 , and did revenues of $9.5 Million

I think with 30 million unit capacity between in house and co packers by end of 24 revenues should be significantly higher than $38 million revenue, as they already had capacity of $9.5 million revenue last Q which is a run rate of $38 Million annualized.

What do you think of this now. Is it even better buy at these prices?